USD/JPY, AUD/USD: Weekly Forex Currency Pair Analysis

The US Dollar regained its strength after being sold earlier in the week, while the Australian Dollar weakened and the Japanese Yen still appears likely to need protection from the Bank of Japan.

The difference between success and failure in Forex/CFD trading will most likely be determined by the assets you select to trade each week and in what direction, and not by the precise methodology you employ to identify trade entry and exits.

Therefore, at the beginning of the week, it is advisable to take a broad view of market events and how they are influenced by macro fundamentals, technical considerations, and market emotion. There are now very powerful market trends that may be exploited economically. Continue reading for my weekly analysis.

Fundamental Analysis & Market Sentiment

In my previous article dated 2 October, I predicted that the best trades for the week would be:

- The short position in the NZD/USD currency pair. The price increased by 0.17%, resulting in a little loss.

- Long the currency pair USD/JPY. The price increase of 0.45% is a tiny gain.

These transactions yielded a modest total average gain of 0.14 percent.

The news is dominated by what appears to be an emerging consensus at the US Federal Reserve over a hawkish course, following significant speculation about a probable dovish flip earlier in the week. Recent Fed member remarks suggest that the Fed is likely to act by continuing to raise interest rates to 4.50%, maintaining them there while inflation is examined further, and being prepared to raise rates further if inflation persists. This developing consensus has strengthened the U.S. dollar, driven the 2-year Treasury yield to challenge its recent multi-year high, and sent stock markets sharply down throughout the course of the week, culminating in a major loss on Friday.

|

👉 Top THREE Award-Winning Brokers in 2022 👈 |

The good US employment figures released on Friday underscored that the US economy is still relatively robust, making it more probable that more rate rises would be necessary shortly and bolstering the bearish argument in stock markets.

OPEC decided to reduce output by 2 million barrels per day, which drove up the price of WTI Crude Oil.

Following Russia's takeover of Crimea and President Putin's strong speech, global attention has returned to the conflict in Ukraine as Ukrainian forces appear to have successfully targeted a strategically vital bridge connecting Crimea to Russia. As with President Biden's stern warning about implied Russian nuclear threats and last week's North Korean missile launch, this may potentially contribute to the strengthening of risk-averse attitude.

The following is a summary of the significant economic data releases from the previous week.

US Non-Farm Employment Change, Unemployment Rate, and Average Hourly Earnings — a net 263k new jobs were created, above the 248k projected, while the unemployment rate surprisingly dropped from 3.7% to 3.5%. As anticipated, average hourly wages climbed by 0.3% month over month.

Swiss CPI (inflation) – this came in lower than anticipated, indicating a 0.2% month-over-month fall when a 0.1% gain was anticipated, offering optimism for a reduction in inflation across Europe.

The US ISM Services PMI report came in little higher than anticipated.

The US ISM Manufacturing PMI report was slightly lower than anticipated.

RBA Cash Rate & Rate Statement - the RBA increased rates by just 0.25% when a hike of 0.50% was generally anticipated, pushing the Australian dollar down throughout the course of the week.

RBNZ Official Cash Rate & Rate Statement — as anticipated, the RBNZ left rates unchanged.

US JOLTS Job Openings - this information was worse than anticipated.

OPEC Meetings — OPEC decided to reduce daily output by 2 million barrels, which was double what was anticipated.

The figures were far better than anticipated, with the jobless rate lowering from 3.7% to 3.5%.

Last week on the Forex market, the New Zealand, Canadian, and US Dollars shown relative strength. The Australian Dollar is the currency with the lowest purchasing power.

Global coronavirus infection rates climbed last week for the first time since July, although the rise is minimal and the total number of infections remains low. Austria, Finland, Germany, Italy, Liechtenstein, Micronesia, Singapore, and Taiwan are the only countries experiencing large increases in newly confirmed coronavirus infections.

The Week Ahead: October 10th – October 14th, 2022

The following week is expected to witness further market volatility, with the US CPI report having the most dramatic potential. The following are forthcoming releases, in order of expected importance:

- US CPI (inflation) statistics

- FOMC Meeting Transcripts

- UK GDP

- Data on the US Producer Price Index

- US Retail Sales statistics

- Initial US UoM Consumer Sentiment

Monday, October 10 is a holiday in the United States, Canada, and Japan.

Technical analysis

U.S. Dollar Index

The weekly price chart below reveals that the U.S. Dollar Index produced a bullish hammer or pin candlestick that ended around the range's high. In addition, it rejected what appears to be a new support level converging with the extremely large round figure 110.00. These are bullish indicators, and the long-term trend is unquestionably quite bullish.

|

👉 Keep Pushing Your Profitable Trading With 👈 |

The Dollar was somewhat volatile in the previous week, but it has now gathered sufficient strength to be gaining practically everywhere.

Bulls may have a minor cause to be cautious, given that last week's closing was not a new high and there was a significant sell-off from the 114.00 region earlier in the session.

During the following week, it would be prudent to pursue exclusively long positions in the US Dollar. This is a highly potent, long-term bullish trend in the most major Forex currency.

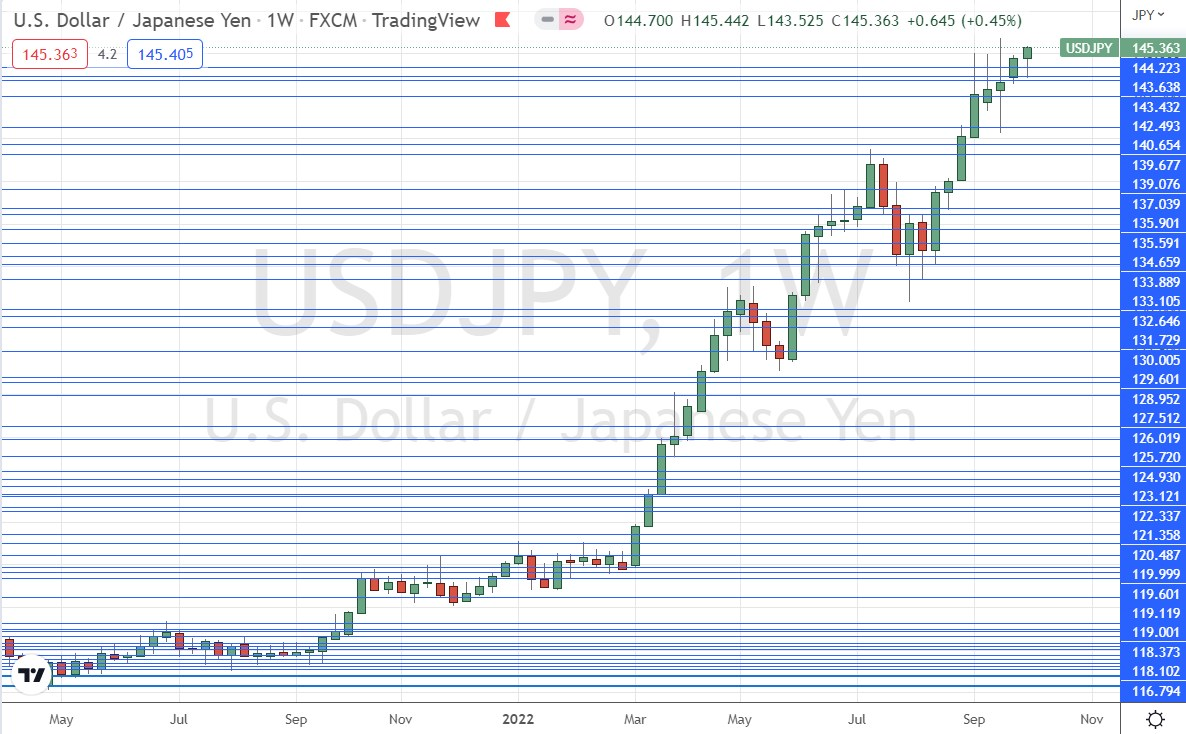

USD/JPY

The USD/JPY currency pair printed another bullish candlestick last week, resulting in its best weekly finish since 1998. The closing price was identical to the weekly peak. There have been eight rising weeks in a row. These indicators are bullish.

As the US Dollar has recovered momentum, this currency pair is worth monitoring this week. This pair is on a very strong long-term bullish trend, as seen by the price chart below. The difficulty for bulls was that the Bank of Japan did not want the price to rise over 145, so it intervened at this level to prevent any further increase. However, it appears that the price has effectively established itself above the crucial round number of 145, therefore it is possible that the Bank may interfere at a higher threshold.

If the Bank of Japan's involvement fails, or if it decides not to interfere, the price may swiftly hit 150 if it rises dramatically.

AUD/USD

The AUD/USD currency pair printed a rather huge bearish hammer candlestick last week, which resulted in the pair reaching its lowest price since the coronavirus panic of May 2020 and its lowest weekly close in almost a decade. The candlestick closed quite close to its low. These indicators are bearish.

The bearish outlook is backed by the fact that the Australian Dollar was already weak when the Reserve Bank of Australia issued a smaller-than-anticipated rate rise last week, which contributed to the currency's continued depreciation. A bearish tailwind exists.

Despite the bearish outlook, there is a nearby strong resistance level at $0.6327 that might hamper bears. If the price falls below that level, it will be a very bearish indicator.

The Australian Dollar is now the second-weakest major currency on the Forex market, after the Japanese Yen, however unlike the Yen, it is highly doubtful that its central bank will intervene to boost the currency.

Bottom Line

The biggest chances on the financial markets this week are expected to be found by selling the AUD/USD currency pair and carefully buying the USD/JPY currency combination, which remains susceptible to intervention by the Bank of Japan.

More News: India's foreign exchange reserves will keep falling. |